Johnathan Ransom, Managing Director, Investment Management & Operations, is the focus of this months interview, representing LoanBook's management team.

1. What is your role in LoanBook?

My title is Managing Director, Investment Management & Operations which means that I am primarily responsible for developing and overseeing business processes, systems and controls. In practice, we have a very capable team with a huge amount of experience, which means that I can focus my attention on those areas that we need to improve. I have a background in operational performance improvement at the consultancy firm, Ernst & Young, so we like to do things right.

My next big task is to prepare LoanBook for the regulatory changes that we are soon to be subject to; a development that is very exciting for our industry and that we are fully embracing, having been closely involved in its development.

2. What goes through the mind of an Englishman to start a project in Spain?

I am very fond of Spain as a place to both live and work. I think that there is a huge opportunity for us to help improve the efficiency and effectiveness of the financial markets in Spain. LoanBook’s crowdlending, or peer-to-peer, model is one that is being used to great success in the UK and US and there is every reason to expect it to be as beneficial to businesses and investors here.

3. What did you learned during your tenure in large firms such as Ernst & Young, Invesco and GPT Halverton that can be applied in such an innovative project as a crowdlending platform?

At Ernst & Young I learnt how important it is for businesses to provide a service that their clients want, at Invesco the importance of getting the right balance between risk and return and at GPT Halverton the benefits of openness and transparency. We try to apply each of those principles to LoanBook’s products and services.

4. Is alternative financing a passing trend?

If economies are starved of alternative sources of finance then they will be much less efficient for it. I believe that borrowers and investors should have a choice of products and services and should not be limited by those that are offered by banks, which has traditionally been the case, to a large degree, in Spain. So, provided Spain continues to work towards developing competitive markets (a core objective of the European Union in its desire to develop and sustain an internal market where competition is free and undistorted) I think that ‘alternative finance’ is here to stay.

Now, alternative finance can take many forms. But I truly believe that the principles that we adopt as part of the peer-to-peer finance model will make our sector sustainable, as those principles of fairness, transparency and trust are ones that should stand the test of time.

5. How would you describe crowdlending in 140 characters?

Crowdlending is the financing of businesses, individuals or projects from multiple sources of capital. The crowd element refers to multiple sources pooling resources and sharing risk. The lending element refers to the fact that those resources are put to work in the form of a loan, on which interest is paid, thus generating a return for the ‘crowd’, and helping the borrowing business grow in the process!

6. In your opinion, what are LoanBook’s key characteristics?

LoanBook is made up of a group of individuals, each with a lot of experience in the traditional world of finance, fixed-income investment, technology and customer service, who are striving to play a part in restoring trust in financial markets by helping to empower investors and borrowers alike. We are characterised by our desire to make a sustainable change for the better and our commitment to do it in the best interests of our customers.

7. What are the main advantages of crowdlending over traditional banking?

I mention some of the benefits previously. Others include:

- Commission transparency: our revenues are based on a simple, transparent fee linked to the service we provide. We do not make profit by putting client’s funds at risk by utilising them for creative financial purposes.

- Disintermediation: crowdlending puts the end user of capital together with the source of capital, which means that the lender is empowered to make their own decision based on their own investment goals, rather than paying someone else to do it for them.

- The marketplace model, where investors can influence the interest rate on the loan, is efficient and transparent, removing conflicts of interests that often occur when a third party is in control of other people’s capital and the decision to lend.

8. What are your hobbies? Do you have any recent recommendations?

As an Englishman in Spain I am still obsessed with sitting in the sun, particularly at this time of year when it is wet and cold at home – I am making up for years of sun deprivation! But it’s not really a hobby, so combine sun with skis and fresh snow and you have my recommendation!

.jpg)

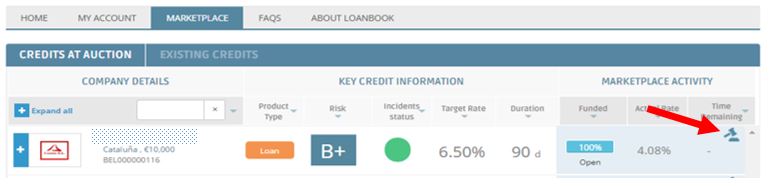

The bid is currently competitive and would be accepted if the auction were to close given other bids in the auction.

The bid is currently competitive and would be accepted if the auction were to close given other bids in the auction.

The bid is not currently competitive and will be rejected if the auction were to close given other bids in the auction.

The bid is not currently competitive and will be rejected if the auction were to close given other bids in the auction.

.jpg) The bid is partially competitive, meaning that if the auction were to close a proportion of the bid would be rejected given other bids in the auction.

The bid is partially competitive, meaning that if the auction were to close a proportion of the bid would be rejected given other bids in the auction.